What is Medicare Supplement Plan N?

Medicare Supplement Plan N is one of the ten standardized Medigap plans. Although one of the newest plans available, Medicare Plan N is quickly becoming a favorite with people aging into their Medicare benefits. This is particularly true of people accustomed to sharing healthcare costs with their employer’s group health plan.

Medicare Supplement Plan N Explained

Medicare Supplement Plan N works with Original Medicare (Part A and Part B) to cover the cost gaps. Also known as Medigap Plan N, this plan covers all of the major gaps (i.e., deductibles, coinsurance, copayments, blood, and foreign travel emergencies) that traditional Medicare does not cover, but costs less than more comprehensive plans because you share some of the costs when you see your doctor. This is why the plan is gaining popularity.

Find Plans in your area with your ZIP Code

To best understand Plan N, and all of its benefits, you first need to get a complete picture of the gaps in Original Medicare. Although Medicare helps cover all of your major medical expenses, it only pays about 80% of the total cost. Without a Medigap insurance policy, you are left to pay the remainder out-of-pocket, including:

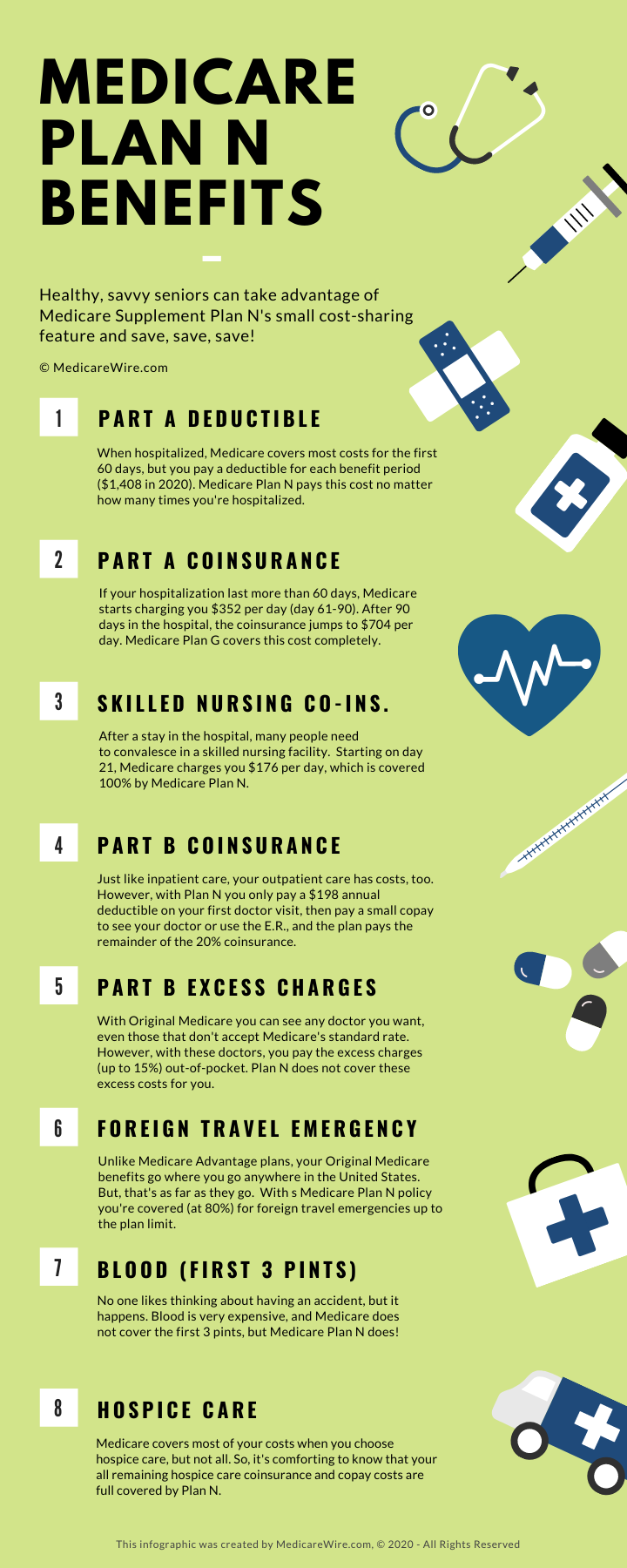

- Medicare Part A Coinsurance & Hospital Costs

- Medicare Part A Skilled Nursing Facility Coinsurance

- Medicare Part A Deductible

- Medicare Part A Hospice Care Coinsurance or Copayment

- Medicare Part B Deductible (annual)

- Medicare Part B Coinsurance or Copayment

- Medicare Part B Excess Charges

- Blood (first 3 pints)

- Foreign Travel Emergency

Some of these costs, such as the Medicare Part B deductible, are minor. However, the Part A deductible, at $1,408 per benefit period (2020 rate), is very expensive. Medicare Plan N helps pay all or part of these costs except the Part B deductible and Part B excess charges.

Medicare Plan N Coverage

The reason a Medigap Plan N policy saves its beneficiaries so much money is that policyholders share some of the most common costs. For example, if you have a Plan N policy you pay a small copayment when you see your doctor (up to $20) and when you use the emergency room (up to $50). With other plans, these Part B costs are paid at 100%, and the monthly premiums are higher, too. This is one of the reasons Plan N policies work so well for healthy seniors. If you rarely see your doctor, because you don’t have any chronic health conditions, why pay for coverage you don’t need?

Think of it this way, if you’re not prone to getting into car accidents, why pay for a $100 collision deductible year after year when a $500 deductible will save you thousands of dollars between collision claims? Medigap plan deductibles and copayments work the same way. If you want to save money, and you’re healthy, get a policy that covers the big costs and pay the small incidentals out of pocket, including Part B excess charges.

Medicare Part B excess charges arise when you use a doctor or specialist that is Medicare-approved but does not accept Medicare assignment. That simply means they do not accept Medicare’s standard payment amount. Medicare allows these doctors to add up to 15% to the bill, but you pay this “excess charge” amount, not Medicare.

Find Plans in your area with your ZIP Code

If you have a Medigap policy that covers excess charges you don’t have to worry about it, but these plans cost more. Medicare Plan N does not cover excess charges, so you’ll pay this cost out-of-pocket when you choose a doctor that does not accept Medicare-assignment.

To recap, here are the costs not covered by Plan N:

- The Medicare Part B Deductible

- Medicare Part B Excess Charges

- A $20 (max) Doctor Visit Copayment

- A $50 (max) E.R. Copayment

Medicare Part N covers all other gaps in Original Medicare, including 80% of foreign travel emergency costs, up to $50,000, after you pay a small copayment.

Medicare Supplement Plan N vs. Plan G

It’s natural to do a Medicare Plan N vs. Medicare Supplement Plan G cost and coverage comparison. Like Plan N, Plan G does not cover the Part B deductible. That means that the only real difference between these two policies is what you pay to see your doctor and to use the E.R., and coverage of excess charges.

For healthy people who don’t have a family history of chronic illnesses as they age, a Plan N Medicare supplement is a great way to save a lot of money without taking a big risk. And that’s really what insurance is all about, mitigating financial risk.

Plan G is the better option for people who see their doctor or a specialist on a regular basis. Plan N is the better option for people who rarely see their doctor for anything other than an annual checkup and want to save money. Both plans offer extensive coverage for what matters most, your inpatient and hospitalization costs.

Medicare Plan N vs. Plan F

Everything said above about Plan N vs. Plan G holds true for Plan N vs. Plan F except for one thing. Medicare Plan F does cover the Part B deductible. A Plan F Medigap policy is the only plan that covers all of the gaps in Original Medicare, and it’s also the most expensive. Is it the best plan? You bet it is, but you pay for the privilege of first-dollar coverage.

First-dollar coverage means that you pay nothing to see your doctor or to use any other Medicare-approved services. With Medicare Plan F, you never have a bill because Medicare pays first and your Medigap policy pays the rest. This is not true with Medicare Plan N.

With a Plan N policy, you pay your Medicare Part B deductible on your first doctor visit. Thereafter you pay up to $20 to see your doctor and up to $50 if you need to use the emergency room. All other costs, except excess charges, are covered by the Plan N policy, just like they are with Plan F. The big difference is the cost. Plan N policies are often 40% less than Plan F policies, depending on where you live. In high-cost of living areas, the savings are often more.

Deciding which plan is best for you is all about taking a good look at your health and your financial situation. For assistance making this important decision, call 1-855-728-0510 (TTY 711) and speak with a licensed HealthCompare insurance agent. There’s no obligation, and they offer more plan options than any other national agency.

Call 1-855-728-0510 (TTY 711) for plan assistance.

If you qualify for Medicare and don't know where to start, MedicareEnrollment.com, an independent HealthCompare insurance broker, has licensed insurance agents who can help you with your Medicare enrollment options, Mon-Fri, 8am-9pm , SAT 8am-8pm EST.